Early Findings in the Tokyo Stock Exchange

Japan has been what is termed a “value trap” for years. The companies listed there had always traded a huge discounts to book/net asset value/ earnings while stock piling cash on their balance sheet. No real activism could take place because a lot of companies in Japan had “cross-shareholdings”, where different Japanese companies owned stakes in other Japanese companies, effectively blocking any potential activist from taking a position and agitating for better corporate governance or capital allocation policies.

However, the Japan of yesteryear is completely different from the Japan of today as the country has undergone a renaissance of corporate change the past few years. In 2022, the Tokyo Stock Exchange reorganized from 4 market sections into 3: the TSE Prime, Standard and Growth. The Prime market is for companies that have large market caps, investable to many institutional investors and good corporate governance with an open dialogue with investors.

You can read about the listing requirements for the other 2 segments here.

Then in 2023, the Tokyo Stock Exchange put out a paper titled “Action to Implement Management that is Conscious of Cost of Capital and Stock Price” for companies in the Prime and Standard markets that pushes the companies to disclose their cost of capital and if they are trading under 1x price-to-book, to discuss the reasons why and plans to get it up to 1x. The Japan Exchange Group has put out Case Studies for the Prime and Standard markets on companies that have disclosed their plans and what effective communication from companies should look like. And they even put out a list of companies that have disclosed or submitted their plans and update it monthly.

So what does this all mean?

It means in Japan there are currently hundred of companies trading at depressed valuations, with overcapitalized balance sheets on low earnings multiples that have the “largest activist” on their back to act as a catalyst to realize full value or near full value for their shares: the TSE and the Japanese government.

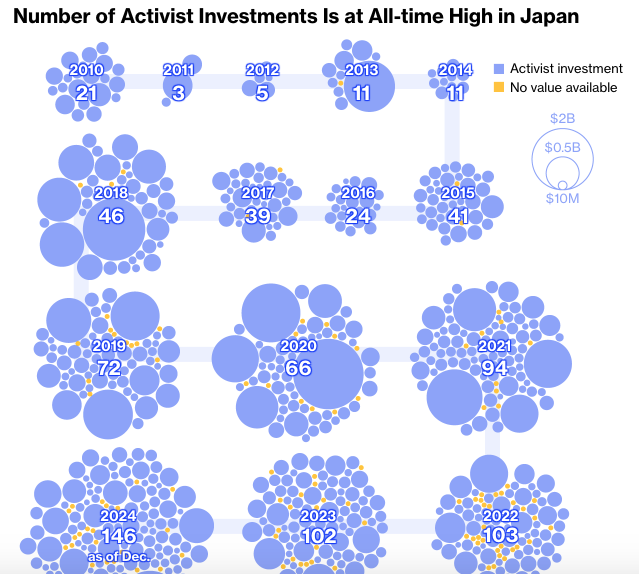

Not to mention that out of the top ten activist funds in 2024, a large portion of their activity was focused on Japan:

Strategic Capital, Oasis, Dalton Investments and Murakami Funds all have activist positions exclusively in Japan I believe. The number of Japanese activist engagements is at an all time high in 2024 as well:

You can see that the Tokyo Stock Exchange new guideline implementations and the activists are making real capital allocation changes as Japanese buybacks were at an all time high in 2024:

Management buyouts are also at the highest levels since 2011 and the Tokyo Stock Exchange is looking to change the Corporate Code of Conduct that will require firms to improve disclosures around the assumptions of how management teams arrive at their buyout prices. The companies are also being told to reduce and sell off their cross-shareholdings of other companies as these inter-company “investments” reduce the company’s overall capital efficiency and promote poor corporate governance as these friendly shareholders won’t hold the management team accountable.

I’ve started to do a bit of digging and some of the companies that I’ve looked at so far seem egregiously cheap (no position in any of these yet):

The Kaneshita Construction Co., Ltd. (1897)

The company is engaged in the construction industry and sells asphalt products and other construction materials as well as operates a conveyor belt sushi restaurant business. If I were to show you the balance sheet and income statement and had you guess what they were worth, I bet many would be off by a large percentage. This is the balance sheet:

And then the income statement:

If you just take the total cash of ¥8.8 billion plus the investment securities of ¥8 billion less all liabilities of ¥3 billion, you get ¥13.8 billion in value with out taking into account any other asset or the operations of the business. If you calculate the NCAV (current assets plus LT securities less all liabilities) your value would be about ¥17 billion. If you use true NCAV (CA - CL), the value is ¥9 billion. And just using book value, the value is ¥18.8 billion.

This company currently trades in the market for ¥5.6 billion (¥2,652 x 2.1m shares). Which means it’s trading a 0.3x book value, with that book value made up of mostly cash and securities. And oh ya, the company has been consistently profitable the past few years. At least 11% of the shares are owned by the Kanashita family with the remaining large chunks owned by Japanese financial institutions. The company pays a paltry 50/share dividend and has announced a 3% share buyback which is hugely accretive because the company trades so cheap.

Takahashi Curtain Wall Corporation (1994.T) - Takahashi has the number one market share in the Japanese precast concrete curtain wall industry. It has been profitable the last 5 years with various swings in income levels.

It’s stock is currently ¥470/share and there are are 9.55 million shares outstanding for a market cap of ¥4.48 billion. It has ¥1.028 billion in cash and ¥222 million of securities against total debt of ¥1.326 billion so EV is ¥4.556 billion. The past 6 year average EBIT is ¥790 million for a trailing 5 year average of 5.8x EV/EBIT. However, they have tons of other building, land and investment property value on the balance sheet for a total book value of ¥10.772 billion which means it’s trading at 0.41x book value. ¥98 million of the securities on the balance sheet is Sumitomo Realty Development which is currently being targeted by Elliot. About 30%-40% of the shares are held by the Takahashi family.

The Torigoe Co., Ltd. (2009.T) - Sells flours and other food products in Japan. With a share price of ¥825 and shares outstanding of 26m, the market cap is ¥21.5B. Torigoe has ¥10.3B in cash and ¥13.4 billion in short term & long term securities against total debt of ¥3.2B which implies an enterprise value of ¥1 billion. Meanwhile the company did ¥1B of operating income in each of the last 2 years. Are they overearning? I don’t currently know. But trading at trailing 1x EV/EBIT is absolutely dirt cheap and this doesn’t take into account the 10B in buildings and land. Of course there are some liabilities totalling ¥9 billion but book value is ¥35.9 billion so it’s trading at 60% of book. There doesn’t seem like there is a controlling shareholder as just 5% increments sit in certain Japanese financial institutional hands.

Heian Ceremony Service Co., Ltd (2344.T) - Has 4 different segments: 1) funeral services where it operates about 50 funeral halls and parlors, 2) two wedding facilities in their wedding segment, 3) a mutual aid business and 4) a nursing care business. Stock price is ¥800, shares outstanding of 12.3m for a market cap of ¥9.84 billion. For that price you get ¥7.4B in cash, ¥2.5B in securities with no real true debt (using the most recent 3Q report) so essentially nil or negative enterprise value. They did ¥1.5 billion in operating profit last year. Their total assets of ¥33.7 billion is made up of mainly land of ¥10 billion, cash of ¥7.4 billion and buildings of ¥6.3 billion. Against total liabilities of ¥12.69 billion, book value is ¥21 billion which means it’s trading at 0.47x book. Another ridiculously cheap stock.

What I’m Looking For

I am sure there are hundreds more like these which brings me to the point of what I’m going to look for when I build my basket up of these companies. I’ll be looking to add about 5-15 stocks based on the following factors/rankings:

1) Degree of cheapness/undervaluation

2) History of profitability

3) Open register/activist involvement

4) Liquidity

5) Business quality

6) Low debt levels

For companies that fit all of these criteria, they’ll represent a larger portion of the basket compared to other companies that don’t.

Some other good sources of material

Neuberger Berman 2023 White Paper

Dalton Investments - Price to Book is Back?

ACGA Open Letter: Strategic Shareholdings in Corporate Japan