A Tetragon of Catalysts

Trading at a significant 57% discount to management’s NAV of 35.43/share with potential catalysts on the horizon to unlock this value.

Note: This write up was based on a $15.5 stock price and it is currently sitting at $15.05. Some of the numbers will have changed due to this but the thesis still remains.

Tetragon Financial is a closed-end investment fund that trades on the Euronext and LSE at a significant 57% discount to management’s NAV of 35.43/share with potential catalysts on the horizon to unlock this value. Tetragon has limited downside based on hard NAV and huge upside optionality depending on the event path that can range from 61% - 234%+. This is a low risk, highly uncertain bet, in my opinion, based on the range of options management can take this. Some highlights of the investment are:

Potential sale of their largest holding, Equitix, that would equate to a $6 per share NAV uplift or $16/share in cash added to the balance sheet vs a current $15.5 stock price.

Buyback/tender offer from proceeds of sale at significant discount to NAV.

Ripple Labs IPO, where Tetragon holds a 2% investment and by my calculations, owns an indirect “look through” XRP token value of $23.46/share

Other potential asset sales and returns of capital

This is one of the more interesting set ups I’ve seen recently. On top of the catalysts, you collect a 3% dividend while you wait.

History

Tetragon invests in different asset classes and IPO’d in 2007 at $10 a share. The stock has pretty much traded sideways at that price since. It has a checkered history starting a couple of years after their IPO. In the early 2010’s hedge fund manager Leon Cooperman sued and released some letters to the board. If you want to read the lawsuit you can here. The gist of it was executive pay was too high, no high water mark on the performance fee calculation, disagreements on capital allocation and the main one: Tetragon founders sold Polygon Management LP, in which they were also founders in, to Tetragon for shares of Tetragon, only to have Tetragon than announce a $150 million buyback the same date. The valuation for the purchase of Polygon wasn’t released, shareholders didn’t get a vote and the whole process was done in the dark with related party conflicts. The lawsuit was eventually thrown out.

There is also the fact that during the GFC, management took down their NAV (as mostly everything was down then) but double dipped on performance fees on their way up as the NAV was written back up as a result of the no high water mark.

Both of these events have left a stain, in my view, on the company which is why it trades at such a large discount to the underlying NAV now and the past decade.

What’s changed vs what hasn’t?

For one, management has actually compounded NAV at a decent clip of about 11% at the same time earning ROEs at the same rate.

When Tetragon first started, the large majority of NAV was made up of a portfolio of CLO’s and bank loans. Today, the bank loan and CLO portion of the portfolio only make up 5%, with ownership of asset management, hedge funds and venture capital comprising over 50% of NAV now. This is a breakdown of their current NAV:

Insider ownership has gone from 11% a decade ago to now sitting at 40%. The lawsuits have all been settled and are now a thing of the past. The hurdle rate to earn their incentive fee is now a larger percentage as in years past it was based on LIBOR + 2.6% where LIBOR was under 1% or equal to it. Now it is based on SOFR + 2.7% but rates are a lot higher today so today the hurdle would be about 7% compared to 3%-3.5% a decade ago.

However, management is still paid a 1.5% of NAV fee and there is still no high water mark. The shares that any shareholder buys are also non-voting shares as in the past too.

Why does this opportunity exists?

If you mention Tetragon to most investors, I am sure they will roll their eyes. Many will remember the lack of a high water mark for the incentive fee or the fact that when you purchase shares, your shares are non-voting. Both are valid reasons and why there is such a large discrepancy between price and NAV. These two reasons are certainly enough to produce an “ick” factor associated with this investment. If you look at the Association of Investment Companies webpage (350 members of the closed-end investment industry in the UK), Tetragon is on the last page when sorted buy price to discount from NAV.

Some secondary reasons creating the opportunity are:

The company reports in USD, trades on the Euronext and LSE and is Guernsey domiciled.

Closed-end investment funds should trade at a discount to NAV

The market doesn’t believe management’s stated asset value

There is a very fatigued shareholder base that has sat on dead money for the past decade and only until the past few months has the stock had a very positive reaction causing the current set up.

Current set up

Thesis #1 - Sale of Equitix

Reuters had a report out in October that Tetragon was in talks to sell Equitix, in which it has a 75% stake in and represents 26% of NAV i.e. their largest holding. The report went on to cite that the value could be 1.5 billion pounds based off of 11 billion pounds of AUM (US $13.8B). Equitix owns some unique infrastructure assets that should be highly coveted by large asset management firms like the contract to operate and maintain the M25, a major highway that surrounds London, or the High Speed 1 30-year contract to operate UK’s high speed rail plus many more.

How likely is the sale? I would give it greater than 50% odds as it was reported by a very creditable source and also confirmed by the company, amongst possibly other potential asset sales. The only reason the company confirms this is to let other bidders know that they are accepting offers or shopping the asset as generally companies don’t comment on press report speculation.

A sale price of 1.5 billion pounds converts into US $1.936 billion. Using a 75% ownership ratio as the 81.48% given in the financials is a little unclear exactly if they receive that full amount, Tetragon would receive US $1.452 billion, which means there would be a value uplift of US$529.6 million to NAV based off of reported NAV for Equitix of US$922.4 million on Dec. 31, 2024. This results in an extra $6/share in NAV uplift or brings on $16/share of cash on the balance sheet, which is just a bit more than where the stock trades today. Even though the company purchased their stake in Equitix for US $208 million, from my understanding of Guernsey tax law there are no capital gains tax and would therefore not have a taxable event.

The infrastructure space has been ripe for deals. BlackRock bought Global Infrastructure Partners for $12.5 billion, which held $100 billion in AUM, for a percentage of 12.5% AUM. CVC Capital Partners just bought infrastructure manager DIF and General Atlantic bought Actis. All these deals could have been a potential trigger for Tetragon to solicit bids and test the market

What could the potential value of Tetragon trade at if they sell Equitix? Based on using 60% price to NAV, it could be worth $25 for upside of 61%. The stock has historically traded at 50% of NAV for the past 10 years but I would argue that a company that’s compounded NAV at 11% since IPO and is willing to sell their largest component of NAV for cash , and maybe return that cash, could see a decrease in the discount from price to NAV. Even if you use 50% there is still a bit of upside.

Thesis #2 - Explore return of capital via tender or special dividend

If/once Equitix is sold, I believe Tetragon could look to make a tender offer using the proceeds at a significant discount to NAV. Management and Tetragon employees own about 40% of the company and would be highly incentivized to see the stock price increase now. What is the use of owning such a large chunk of a significantly undervalued company if you cannot sell your shares for their true fair value? I am assuming the tender occurs at $25 because that’s the value I have if Equitix is sold. It could, if it occurs, happen at levels below $25 which would be even more accretive to NAV. But assuming a tender is done at $25, it could result in 80% upside.

Thesis #3 - Potential IPO of Ripple Labs

This is where the thesis gets really interesting. I’ll preface by saying that I am in no way a crypto expert but I like situations with extreme optionality on the upside, even if there are different event paths that could occur. The late grate Michael Price called this the steak and sizzle approach. Focus on the steak and get the sizzle for free.

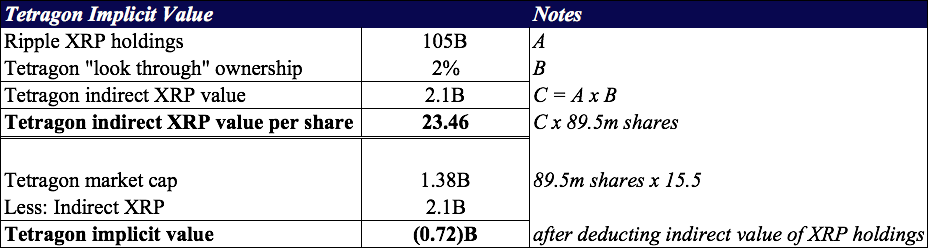

In 2019, Tetragon made a Series C preferred equity investment in Ripple Labs for $150 million with the option of Ripple redeeming their investment if it was ruled that XRP was a security on a go-forward basis. The SEC sued Ripple in 2020 stating they had been issuing unregistered securities from the sale of XRP, which led to Tetragon suing Ripple to redeem their investment as a result of the SEC lawsuit. Tetragon’s suit was dimissed and Ripple decided to buyout the Series C preferred back anyways in 2021. Tetragon then purchased Series A and B preferred of Ripple on the secondary market. While they have never disclosed the price paid or terms, there have been reports that they own about 2% of Ripple. Although not a perfect method, triangulating what Ripple is carried at on Tetragon’s balance sheet vs Ripple valuation in 2024 comes to roughly 2%:

What’s interesting about their Ripple investment though is that Ripple in January 2024 owned $25 billion worth of XRP tokens on their balance sheet at a rough price of $0.5/token when they did their tender offer for $11.3 billion last year. This meant they were buying back shares at under a 50% discount to net asset value and I believe they made another tender in 2024. And now one year later, the XRP price has gone vertical:

Sitting at just around $2.3, their XRP tokens are now worth more than $100 billion, thanks to a nearly 5-fold increase in price and the CEO of Ripple thinks the original $11.3 billion valuation of Ripple is “very outdated”. The drastic price increase is as a result of the friendly Trump administration coming into office, the resignation of Gary Gensler who was antagonistic to Ripple, Ripple only having to pay a $125 million dollar fine which was substantially below the $2 billion the SEC wanted from their lawsuit and the SEC recently approving bitcoin ETFs. Not to mention a potential US Strategic Reserve for purchasing cryptocurrencies that could come into affect.

Ripple’s balance sheet isn’t public so we can’t see exactly how many tokens of XRP it holds but its around 46 billion against a total supply of 100 billion according to various news outlets. At today’s price of $2.3, Ripple owns about $105 billion XRP on balance sheet. At Tetragon’s current stock price, the “look through” ownership of their XRP holdings are about $23.46 which means Tetragon’s implicit value less their holdings is negative 720 million. Stated another way, an investment in Tetragon today means you are receiving about 3B of assets for a negative $720 million.

GAM Global Special Situations Fund has noticed the same implicit value in SBI Holdings, which is a Japanese financial services company that owns 8%-9% of Ripple and based on their look-through holdings, is trading at a negative market cap as well. They recently sent a letter to SBI you can read here. They want SBI to publish a daily figure of SBI’s lookthrough XRP holdings and to establish a public XRP coin buying program buy purchasing the coins outright to close the gap to NAV, similar to what Microstrategy has done in the US.

And Ripple itself is essentially doing somewhat of a reverse Microstrategy approach. Microstrategy issues equity at a premium to NAV and buys bitcoin whereas Ripple is just tendering for shares at a severe discount to NAV and could/should possibly sell some on balance sheet XRP and use it to repurchase more shares.

So what is the likelihood of Ripple going public and potentially releasing all of this value? Last January Ripple was looking to go public outside the U.S. because of the hostile SEC and decided to put it on hold. Since then, Gary Gensler is no longer the SEC chairman and the Trump administration has been viewed as extremely favourable to the crypto industry. Trump even issued his own coin days before he entered the white house with the first lady following suit. The CEO of Ripple has stated that going public wasn’t prioritized previously because of the prior SEC administration. With that administration now gone, experts are predicting late 2025 to 2026, potentially once the lawsuit with the SEC is finalized. I have no unique insight into when this could occur but view it as extremely positive for this investment (maybe not for society overall) that the administration is very pro crypto. While Ripple does trade on certain private markets online, coming to a precise valuation is near impossible due to no real business numbers being available. Just using a valuation of $15B, almost a 50% increase from their tender, gets to an overall stock price of Tetragon up 84%.

While the above valuation is just valuing Ripple’s potential business based on a gain from their last tender of $11.3 billion, this investment can get a bit silly on potential upside optionality if/when Ripple comes public and the market chooses to value it based on their on balance sheet XRP holdings. If the market were to value it just at todays XRP value of $105B, the upside can be quite dramatic.

And if Ripple starts trading like how the market values Microstrategy, at a multiple of their bitcoin holdings, Ripple could be worth a multiple of the 105B on balance sheet crypto holdings. The scenario above doesn’t account for the fact that the XRP token price could increase in value, or that Ripple would most likely be a highly coveted IPO by a lot of retail traders and garner a huge valuation.

Thesis #4 - Other asset sales

There is the possibility of other asset sales on top of Equitix. One of the analysts covering Tetragon thinks the BGO asset could be disposed of in the near term. While this would be viewed favourably by the market (of course depending on price and uses of the cash), it is not a main point to the overall thesis but would be most welcomed.

Potential Value Creation

Management and other executives own about 40% of the company, with the two main founders Reade Griffith and Paddy Dear owning 27%. I think they have done a relatively good job of compounding NAV since inception at 11%. One thing that does bother me is management’s aloofness on how to close the discount to NAV. On the most recent call they said “they don’t think there is a clear silver bullet to closing the discount to NAV”. I lay out some options on what I would do to close the discount at the end of this write up but with the persistent discount to NAV ongoing, upper management have the option of collecting their combined $50-$100m incentive fees per year until they retire in 5-10 years, or they have the option of creating a ton of value right up front. Based on my valuations, this could be the potential value they can create for themselves:

Risks

In all potential deals, there is the possibility of the sale falling through. If the Equitix sale doesn’t occur, it is possible this trades back down a bit and is dead money. I don’t think it should trade back down to 10, it might go down to the 11-12 range based on the markets perception that the company is willing to entertain offers for some of its assets and turn at least some of their investment NAV into cash.

What if Equitix might not get as a high a price as reported? Anything at NAV or above and turning their investment into cash is a win in my opinion as they could still use that cash to repurchase at a significant discount to NAV.

Or what if the company chooses to reinvest any proceeds from asset sales into other investments? While a bit of risk, it wouldn’t be a terrible outcome as management has shown they can grow NAV at a decent clip. However, this wouldn’t allow for larger outsized returns as outlined above in my opinion.

There is also the risk that if a down turn occurs, management can write down NAV, write it back up and double dip like they did in the GFC. I give this situation occurring low odds. Back in the GFC, management owned just loans and CLO’s, assets that were heavily affected by the crisis and most likely deserved to be written down then. Now they own a more diverse set of assets. We’ve also seen during the COVID 2020 market that their NAV actually increased, which should dispel most of this risk. The company could also face a barrage of lawsuits from investors, tainting the investment in the stock even more and thereby increasing the price to NAV of where it trades, in which management owns 40% and not giving them a path to realize their holdings at fair value.

What if Ripple doesn’t IPO or the price of XRP drops? While a lot of the upside of the investment could be tied to a Ripple IPO and their significant holdings of XRP on balance sheet, you don’t need the Ripple IPO to occur to earn a decent return in the stock. While it would be nice for Ripple to IPO and be a highly coveted asset by retailer and institutional investors, if they stay private they can still grow their value without going public. And even if their value doesn’t increase, Tetragon the stock, can still earn a good return if management liquidates some assets and repurchases shares.

Event Path If I Were Management

The first step I would take is currently what mangement is doing. Putting one of your largest holdings on the block and trying to crystalize that value. I would also sell another asset as well for further NAV uplift. Once these sales occur, I would announce a larger tender at a significant discount to NAV in order for NAV/share to grow even further, increasing management’s and investors who choose to stick around ownership further.

The next step, however unlikely, would be to convert the non-voting shares into voting. If management doesn’t sell back into the tender, they could go above 50%, thereby making the newly proposed voting shares semantics as they would now control the voting shares and eliminate some of the discount to NAV. At the same time, instill a high water mark which would further erase some of the discount to NAV. Instead of the high water being just NAV, tie it to some type of performance based measurement of shareholder value like stock price. These two steps I would do after the tender to allow a larger price to NAV gap to exist during the buyback.

Once these are done, start highlighting the Ripple investment and the indirect “look through” XRP that Tetragon now holds. This could show the market that one of the ways to play the Ripple IPO would be by owning Tetragon, thereby increasing demand for the stock.

Disclosure: Long TFG.AS, TFG.LN

Investment Idea: Currency Exchange International

Sometimes investment theses start with GoodCo./BadCo., where BadCo. is sold or spun off to highlight the value of the GoodCo. Currency Exchange International (“CXI” on the TSX and “CURN” over the counter) represents GoodCountry/BadCountry, with the BadCountry being wound down over the next year.

Currency Exchange International - Long

Note: this was written up based off a $15.93 stock price and it is now trading at $15.25.

Jerry Jones Outsized Returns; Interesting Reads

Some key attributes of Jerry Jones’ investments that made him so rich; a couple of interesting reads this past weekend.

I was listening to the Founders podcast episode on Jerry Jones and wanted to jot down some key characteristics of what made some of his investments so great as well as a brief summary of the podcast. I highly recommend listening to it. I wasn’t aware that Jerry’s Cowboys purchase was a deep value turnaround.

Jerry Jones had always wanted to purchase an NFL team. He had told everybody all his life he wanted to. But first he had to make some money to finance it. He made a bit of money when his father sold his insurance company that Jerry helped build and which netted him about $500,000. Since he was extremely hungry to become rich, he then moved to Little Rock, Arkansas and wanted to get into the oil business. His first deal was when he met someone who was shopping an oil deal that everyone had turned down and had said no to. Jerry was the only person who had said yes, while at the time he was selling mobile homes.

The result?

The group hit their first well that was worth more than $4 million dollars. And they kept hitting wells each time they drilled for 15 consecutive times. He ended up selling 1 of his oil production companies in 1976 for $50 million.

What allowed him to make an outsized return on this investment that I think can apply to public markets or any type of investment is 1)When people turn their nose up at it and think it is dumb/crazy, 2) There is an ick factor associated with the investment and 3) Everyone doesn’t want to touch it and says no to it. When any of these characteristics apply to an investment you are being pitched, I believe it would pay to do more work. Or to look for investments that people think are dumb/crazy to invest in to. I don’t mean to go look for huge cash burning non-revenue generating businesses, but real businesses with downside protection that others don’t or can’t touch for whatever reason. A good example wold be General Growth Properties in 2008.

2nd and 3rd Investment

After his first success, in 1980 he decides to drill for natural gas with a partner and they take a shot drilling at 2 wells. One near San Francisco and one in South Eastern Oklahoma. Right away, the production was a disaster as an employee made a half a million-dollar mistake by accidentally dumping cement in the well ruining it at their Oklahoma location. They then invested another $500,000 and moved the drill bit 100 feet and the next day hit a natural gas well worth over $40 million. While this was happening, the San Francisco well was going to be worth $40 million over a two-year period. In total, they made $80 million on their first two natural gas drills.

The last deal he does before buying the Cowboys is extremely interesting. Jerry’s friend was the CEO of Arkansas-Louisiana Gas Company, which is the state regulated utility company. In 1981, Jones forms a new gas drilling company called Arkoma Production Company. He then enters into a deal with Arkansas-Louisana Gas Company (which people say is one of the greatest sweet heart deals of all time) that allows Jones’ company to sell gas to this utility company (which his friend is the CEO of) at a price much higher than what the utility company was currently paying other gas companies for their gas. The deal was for $4.50/thousand cubic feet, which meant Arkoma was getting more than 9x the price that other natural gas producers were selling their product for.

Then in 1985, the natural gas industry was deregulated and the price of natural gas went down significantly. But because of the terms of the agreement between Arkoma and the utility, the utility company had to purchase from Arkoma the most amount of gas it could produce at the maximum legal price. Jones then decides to purchase other natural gas producers that didn’t have this sweetheart deal because he has a guaranteed price he can sell to the utility company compared to what all the other natural gas producers could currently sell at. Thereby buying more supply and selling the gas at the inflated rate. The end result of all of this: the utility company was paying Arkoma $40 million a year for gas it didn’t need. Because this was a terrible deal for the utility company, it decided to purchase Arkoma in 1987 for $175 million. The total value to Jones and his partner based on money taken out of the business and sale price allowed them to pocket over $300 million. These articles here, here and here give a good background of the deal. This leaves Jones with about $90 million in cash at this point in his life.

Cowboys Purchase

The current owner of the Cowboys in 1988 was forced to sell the team because he had a severe cash crisis with all the businesses he owned. The owner was never really interested in owning the team but wanted to own it for the depreciation it threw off to cover his profitable oil business. When he decided to sell, he pitched 75 people who all had said no and financial advisors at the time had said buying the cowboys was “ridiculously overpriced, and financial suicide”. Enter Jerry, who buys the team in 1989 for $140 million. He used all of his $90 million in the bank and borrowed the remaining $50 million at high interest rates.

With that, he got a football team that just recently lost $9 million, couldn’t sell a majority of the luxury suites as only 6 of 188 were sold, attendance dropping 25% from the prior year, and only one home game had sold out.

Within a few years from taking over they were averaging more than $30 million in profits per year and are now doing over a billion in revenue. As of 2024 they were valued at $10.1 billion, earning 112 times his initial $90 million investment.

Here’s how he earned outsized returns on his Cowboys purchase:

Purchased from a forced seller

The owner had shopped the team to 75 other parties who all said no before Jones came into the picture and said yes.

Took advantage of low hanging revenues opportunities.

If you sell the luxury suites in your stadium, you don’t have to share the revenues with other NFL owners as you do the typical ticket revenues. The suites could sell for $400,000 to $1.5 million and after a few years he had 95%-98% of them filled. This turned into $50 million profit just from selling these.

Moved the free press seats that were the best seats on the 50 yard line to the 5 yard line and sold these 50 yard line seats.

There were no ads inside the stadium. He placed ads inside the stadium and sold these ads to local businesses.

At the time they couldn’t sell beer and alcohol at the games. Jerry lobbied and wined and dined the city council to grant him a stadium license to sell alcohol. This turned into $1.5 million to $2 million per game in profit.

Hired sales and promotion people and cut positions that weren’t generating revenue.

His cowboy purchase can be boiled down to a few key characteristics: 1) There was a forced seller, 2) The cowboy franchise is a scarce asset as NFL franchises are rarely if ever expanded. This creates a lack of supply with all demand growth going to the limited franchises in existence and acts as a tailwind, 3) No one wanted it as it was shopped to 75 other parties, 4) Extremely low hanging revenue opportunities that were just common sense to implement.

These key characteristics in his investments are what everyone should be on the look out for and has made Jerry Jones one of the richest men in the world today.

Interesting Reads

A couple of interesting reads this past weekend:

1) Tom Murphy 2000 HBS Interview

2) Ben Graham 1955 testimony before congress

Gulf & Pacific Equities Corp.

An interesting stock I came across to put on my watchlist is Gulf & Pacific Equites Corp. (GUF.V). It’s not something I would invest in now as I would need some sort of catalyst for this idea to work and don’t see it right now.

An interesting stock I came across to put on my watchlist is Gulf & Pacific Equites Corp. (GUF.V). It’s not something I would invest in now but would need some sort of catalyst for this idea to work and don’t see it right yet.

Gulf owns 2 malls, a retail property and a piece of land in Western Canada. All of the assets are owned in small towns. One mall is located in St. Paul, Alberta and is 100% leased with good tenants (Tim Horton’s, Dollar Tree, Mark’s and more). The other mall is located in Cold Lake, Alberta and is not 100% leased but has good tenants as well (Pizza Hut, Sobeys, Taco Bell, etc.). The retail property is located in Three Hills, Alberta and is leased 100% to Dollarama long-term. And then there is a vacant land owned in Merritt, BC which management doesn’t give any value to.

The company began operations in 1999 and this is the income statement the past 2 years:

It looks extremely profitable but the profits the past two years are really as a result of the FV adjustments in the way they mark up or down their properties and run it through the income statement. It is essentially breakeven on an operating basis. But what got me more interested was the balance sheet:

The stock trades at $0.42 with fully diluted shares outstanding of 22,660,685 for a market cap of $9.5m. Right from the balance sheet you can see it is trading for 43% of book value. If you include the FV adjustments as real income (which I don’t) it would be trading at 8x last years earnings. In the notes, management states it recently had appraisals done for the 3 properties as well as completed their own appraisals and the two large malls were worth $48.35m and the smaller location was $2.01m.

The CEO owns 52% of the shares through his investment company Ceyx Properties Ltd. and insiders own a combined 55%. Two other shareholders own another another 28% so the shares are in just a few hands which leaves the remaining 17% shares to the public.

There is a pretty compelling case to be made that this should just be privatized to a larger retail/mall operator:

Reduce public company and management costs. Management and the board are paid just over $400K a year which would drop straight to the acquiror’s bottom line as well as public company/audit costs not included in that $400K number.

Access to lower costs of capital from merging with a larger entity.

Become part of a larger mall portfolio which would reduce business risk as there would be many malls in the portfolio.

The CEO is currently running this company as well as another publicly traded junior gold miner, Plato Gold Corporation and he is also the CEO of Ceyx Properties Ltd.

Gulf & Pacific won’t ever get the appropriate earning/FFO/book value multiple because it is too small and illiquid.

In order for me to get real interested, I would need to see discount to book as well as cheap on an earnings/FFO/cash flow multiple. If the Cold Lake mall can get near or to 100% leased it might get there. Or management decides to liquidate and pay proceeds out to shareholders. Until then I am just going to add it to my watch list.

Disclosure: Stock watchlist

Liquidating Cannabis REIT with a Catch

Two posts ago I talked about “seasoned liquidations” and I just happened to have found exactly that.

Two posts ago I talked about “seasoned liquidations” and I just happened to have found exactly that. Nova Net Lease REIT is selling its main asset, Class A Units of an operating partnership, for $3.71m USD, or $0.50 per share, after undergoing a strategic review. This represents a 456-498% premium to the 30-day VWAP. Nova will then wind down its REIT and subsidiary corporation and make a liquidation distribution to shareholders relatively quickly in the next month or two in the amount of US $0.40-$0.43/unit. In the press release the distribution is to be expected in 30-60 days following the completion of the sale and in the circular it just says first quarter of 2025. This could provide upside of between 12% - 22%. Its trading OTC at $0.3526 as ticker NNLRF and on the Canadian Securities Exchange at $0.375 with ticker NNL.U. The only problem: I haven’t been able to get any order filled as the volume is dreadful so I thought I’d just share it anyways as a good case study for finding inefficient mis-pricings in the smaller market areas. And maybe someone reading this will be able to get a buy in before the distribution.

Nova owned a cannabis industrial investment property as well as a JV that held two cannabis investment properties. This is the organizational chart with what they sold.

From reading the documents, they effectively had a 35% economic interest in the LLC they sold. So after this sale, they are going to be left with Verdant Growth Properties Corp. and the REIT at the top, both of which are going to be wound down. If you look on page 74-75 on the circular PDF, you can see the financial advisor’s liquidation value calculations for the LLC which comes to roughly the distributable amount.

The transaction was announced in November and unitholders held a meeting to vote on the transaction December 20. The shareholders voted to complete the sale and it closed on January 9. Management stated $0.40-$0.43 in the press release was the estimated distribution and in the Fairness Opinion that amount is given as more precisely $0.42/share in US dollars.

Based on the net difference between $0.50 per share and expected payout of $0.42, the estimated liquidation costs are about $596,000, which seems about right for a relatively quick/small liquidation. They also released the CEO when the agreement was entered into and replaced him with the CFO with no additional compensation. Also, not that it matters much, but I don’t think I have seen the financial advisor, or someone who works for the financial advisor, provide a fairness opinion and they themselves own a stake in that company.

The spread is available because the liquidity is tiny. I am a little disappointed I haven’t been able to get my ordered filled but I know there will be plenty more of these to play and hopefully someone can take advantage of the spread.

A-Z on the Canadian Securities Exchange

This January I thought I’d go A-Z on a small backwater exchange here in Canada, the Canadian Securities Exchange. This is the exchange one tier below the TSX Venture, which itself is a tier below the TSX. I downloaded the excel list of companies from the CSE website and started at the top.

The game of investing is turning over the most rocks until you find something that seems extremely compelling. This could come from reading investor letters, investment pitches, running screens, following news flow, etc. But you aren’t going to see what truly are the best opportunities unless you go through every stock on each exchange. The beauty of looking at every stock is that you can than compare it to your existing portfolio as opposed to waiting for investments to come around. The problem with this is it is extremely time consuming and you usually end up finding a lot of junk/unprofitable companies as you can see from my notes on the right below.

While there is no exact tell for what I was looking for when going through each company’s financial statements, I wanted to see actual businesses that were profitable or at least almost profitable with a strong balance sheet. Everything else was an immediate pass. How else can I value a business if there is no real business?

A couple observations

For a country with vast natural resources, Canada has a TON of unprofitable mining companies.

A lot of these companies should probably just be liquidated/not publicly traded.

Going A-Z is never easy and I found myself thinking I should just skip the names that just seem like an obvious pass but if everyone thinks like that there might be some hidden gem.

Once you get into the habit of starting, it can become a bit addicting trying to see each company everyday. At the end of each session I found myself wanting to look at “just one more” which would usually turn into 10 more.

My goal was to do at least one letter of the alphabet each day and I would usually surpass that because some letters didn’t have many companies.

I managed to make a list of at least some interesting companies to keep an eye on and thought I’d share the top 10 companies I thought were the most interesting.

1) ZTEST Electronics Inc.

Develops and assembles printed circuit boards and is currently undergoing a strategic review. Almost doubled revenues from 2023 to 2024 with net income going from $165K to $1.7m. Shares outstanding of 36.5 + 2.7m warrants +1.1m options with a stock price of $0.40 for a market cap of $16.12m. Trading at 9.5 times last years earnings and if they can grow again at the same rate this year, it seems really cheap. Strong balance sheet with cash balance of $2.7m against debt of just over $100K.

2) BioHarvest Sciences

They synthesize plant based molecules and have a market cap of $110m with insiders owning 37.9% of the company. Their revenues and gross margins have exploded the past couple of years. In 2021 they did revenue of $2.1m and gross margins of 31.9%. In the TTM of Q3 2024, they’ve done revenue of $22.4m and gross margin of 54%. Huge growth that is hard to argue with.

The only downside is they are still losing money but on a lesser scale as a couple of years ago. Also, their shares outstanding have gone up as they have raised money to fund the growth. This is one I will be keeping my eye on for when 1) potential profitability will inflect, 2) no need to raise capital anymore, 3) if the valuation makes sense and 4) if I can get comfortable with the business/industry.

3) Eagle Royalties

A junior mining company but it holds 35 royalty interests in certain projects in Western Canada covering different commodities. It was spun off from Eagle Plains Resources in 2023 on a 3 for 1 ratio. Extremely strong balance sheet with total assets of $4.8m with cash comprising $3.5m of that and a note receivable of $1.25m against total liabilities of $303K. Market cap is $6.6m but they just diluted shares from 28m to 57m, with fully diluted 66m. Royalties seem lumpy as they just received one so far this year for $3.75m which turned into net income of $2.9m in the last 12 months. Insiders own 20-30%.

4) Happy Belly Food Group

Seems like an interesting small business. Has a bunch of different brand food locations/consulting and also earns royalty and franchise stream income. Sales have been growing as of September 30, 2024 as they have done 5.2m in past 9 months vs 3.8m last year same period. However, still burning money and diluting but looks like cash burn has come down. Total assets of $9.1m with cash making up $3.6m of it against $3.6m of convertible debt.

5) MTL Cannabis Corp.

One of the rare profitable cannabis companies I’ve seen, although they did lose money in 2023 but they under went a RTO mid 2023. With 117m shares outstanding, 7.7m warrants and 6.5 options, there is a market cap of $48.5m using a stock price of $0.37 (not using the treasury method). While I don’t love the balance sheet of $22.6m debt against $3.2m cash, there is $18.5m of PP&E backing that up as well. Sales have been growing, going from $32m September 2023 last 6 months to $42m September 2024 last 6 months. This takes into account $10m of excise taxes as well and if the government were to change this in the next few years, it could fall right to the bottom line.

Operates 2 segments: 1) Licensed producer that just did $11m in operating income and $8.5m net income past 6 months, 2) CHC segment that did $430K operating income and $100K net income past 6 months as well. On a consolidated basis when taking corporate expenses into account, its 9m operating income and $3.4m net income. Annualize that for the year could be $18m in operating income and $7m in net income against a market cap of $48.5m for 7 times earnings.

6) Namesilo Technologies Corp.

Nice little domain name business run by Paul Andreola. Holds 1.2m in bitcoin investments as well as some other of his investment picks (Atlas Engineered, Ceapro Inc.). Does just over $40m in revenues and is profitable on an operating basis of $3-4m. Only debt is 3.8m convertible and large amount of liabilities is the deferred revenue of almost $30m of a the total $43m in liabilities.

7) Nova Net Lease REIT

I will most likely be writing this up in a couple of days but it is a Cannabis REIT that owns one investment property and a JV that owns two other properties that are profitable. Just agreed to sell most of the assets and liquidate. Stock price of $0.36 with units outstanding at 7.4m, market cap is $2.6m. The book value without making any adjustments to the properties or JV is $12m, which means on my rough math it is trading at 22% of book value. But this could be as a result of them consolidating the JV onto their statements so their true economic ownership doesn’t show through. Granted it is losing some money and burning a bit of cash but the JV is profitable according to the notes in the financial statements.

8) Urbana Corporation

Investment company with a net asset value of $427m or 10.32/share. Currently trading at $6.19 which means it is valued at 60% of net asset value. Investments are made up of both public and private amounts. Public is $202m on balance sheet and private is $297m with some private debt investments of $6m. Management in September was granted by TSX to allow a NCIB to repurchase 10% of the company’s shares which means management agrees it is undervalued. Smart capital allocation to purchase below asset value which would bump up the NAV per share after the buyback. Reading past investment pitches on them, they have always traded at a large discount.

9) ICEsoft Technologies Canada Corp.

Licenses its technology and its SAAS product to businesses and government clients. They do the mass notifications that pop up on your phone if the government needs to let people know of certain emergencies. Seems like losses have come way down and they are near breakeven. Trades at a roughly $5m market cap when taking the warrants into consideration. Annualizing their current quarters revenue, trades for about 2.5 times revenue. The balance sheet isn’t the greatest with only $111K in cash against $1.2m of convertible debt. Not a buy to me as I need a clean balance sheet and profits but one to keep an eye on.

10) Victory Square Technologies Inc.

Investment company with investments made in the tech. sector and consilidates a bunch of their investments on to the financials. Has a market cap of $45.7m but they own a 64% stake in Hydreight Technologies (Ticker is NURS.V) that is worth roughly $60m as the stock has gone crazy the past year. They also own other investments that I am sure are worth more. Could be interesting if they ever try to unlock some of this value.

Honourable Mentions

—> Grown Rogue, Plaintree Systems Inc, Royalties Inc.

I am hoping to do the TSX Venture exchange in February/March. The CSE only has about 771 listings whereas the TSX Venture has I think triple that amount so it will take me a bit longer to do obviously.