A Tetragon of Catalysts

Trading at a significant 57% discount to management’s NAV of 35.43/share with potential catalysts on the horizon to unlock this value.

Note: This write up was based on a $15.5 stock price and it is currently sitting at $15.05. Some of the numbers will have changed due to this but the thesis still remains.

Tetragon Financial is a closed-end investment fund that trades on the Euronext and LSE at a significant 57% discount to management’s NAV of 35.43/share with potential catalysts on the horizon to unlock this value. Tetragon has limited downside based on hard NAV and huge upside optionality depending on the event path that can range from 61% - 234%+. This is a low risk, highly uncertain bet, in my opinion, based on the range of options management can take this. Some highlights of the investment are:

Potential sale of their largest holding, Equitix, that would equate to a $6 per share NAV uplift or $16/share in cash added to the balance sheet vs a current $15.5 stock price.

Buyback/tender offer from proceeds of sale at significant discount to NAV.

Ripple Labs IPO, where Tetragon holds a 2% investment and by my calculations, owns an indirect “look through” XRP token value of $23.46/share

Other potential asset sales and returns of capital

This is one of the more interesting set ups I’ve seen recently. On top of the catalysts, you collect a 3% dividend while you wait.

History

Tetragon invests in different asset classes and IPO’d in 2007 at $10 a share. The stock has pretty much traded sideways at that price since. It has a checkered history starting a couple of years after their IPO. In the early 2010’s hedge fund manager Leon Cooperman sued and released some letters to the board. If you want to read the lawsuit you can here. The gist of it was executive pay was too high, no high water mark on the performance fee calculation, disagreements on capital allocation and the main one: Tetragon founders sold Polygon Management LP, in which they were also founders in, to Tetragon for shares of Tetragon, only to have Tetragon than announce a $150 million buyback the same date. The valuation for the purchase of Polygon wasn’t released, shareholders didn’t get a vote and the whole process was done in the dark with related party conflicts. The lawsuit was eventually thrown out.

There is also the fact that during the GFC, management took down their NAV (as mostly everything was down then) but double dipped on performance fees on their way up as the NAV was written back up as a result of the no high water mark.

Both of these events have left a stain, in my view, on the company which is why it trades at such a large discount to the underlying NAV now and the past decade.

What’s changed vs what hasn’t?

For one, management has actually compounded NAV at a decent clip of about 11% at the same time earning ROEs at the same rate.

When Tetragon first started, the large majority of NAV was made up of a portfolio of CLO’s and bank loans. Today, the bank loan and CLO portion of the portfolio only make up 5%, with ownership of asset management, hedge funds and venture capital comprising over 50% of NAV now. This is a breakdown of their current NAV:

Insider ownership has gone from 11% a decade ago to now sitting at 40%. The lawsuits have all been settled and are now a thing of the past. The hurdle rate to earn their incentive fee is now a larger percentage as in years past it was based on LIBOR + 2.6% where LIBOR was under 1% or equal to it. Now it is based on SOFR + 2.7% but rates are a lot higher today so today the hurdle would be about 7% compared to 3%-3.5% a decade ago.

However, management is still paid a 1.5% of NAV fee and there is still no high water mark. The shares that any shareholder buys are also non-voting shares as in the past too.

Why does this opportunity exists?

If you mention Tetragon to most investors, I am sure they will roll their eyes. Many will remember the lack of a high water mark for the incentive fee or the fact that when you purchase shares, your shares are non-voting. Both are valid reasons and why there is such a large discrepancy between price and NAV. These two reasons are certainly enough to produce an “ick” factor associated with this investment. If you look at the Association of Investment Companies webpage (350 members of the closed-end investment industry in the UK), Tetragon is on the last page when sorted buy price to discount from NAV.

Some secondary reasons creating the opportunity are:

The company reports in USD, trades on the Euronext and LSE and is Guernsey domiciled.

Closed-end investment funds should trade at a discount to NAV

The market doesn’t believe management’s stated asset value

There is a very fatigued shareholder base that has sat on dead money for the past decade and only until the past few months has the stock had a very positive reaction causing the current set up.

Current set up

Thesis #1 - Sale of Equitix

Reuters had a report out in October that Tetragon was in talks to sell Equitix, in which it has a 75% stake in and represents 26% of NAV i.e. their largest holding. The report went on to cite that the value could be 1.5 billion pounds based off of 11 billion pounds of AUM (US $13.8B). Equitix owns some unique infrastructure assets that should be highly coveted by large asset management firms like the contract to operate and maintain the M25, a major highway that surrounds London, or the High Speed 1 30-year contract to operate UK’s high speed rail plus many more.

How likely is the sale? I would give it greater than 50% odds as it was reported by a very creditable source and also confirmed by the company, amongst possibly other potential asset sales. The only reason the company confirms this is to let other bidders know that they are accepting offers or shopping the asset as generally companies don’t comment on press report speculation.

A sale price of 1.5 billion pounds converts into US $1.936 billion. Using a 75% ownership ratio as the 81.48% given in the financials is a little unclear exactly if they receive that full amount, Tetragon would receive US $1.452 billion, which means there would be a value uplift of US$529.6 million to NAV based off of reported NAV for Equitix of US$922.4 million on Dec. 31, 2024. This results in an extra $6/share in NAV uplift or brings on $16/share of cash on the balance sheet, which is just a bit more than where the stock trades today. Even though the company purchased their stake in Equitix for US $208 million, from my understanding of Guernsey tax law there are no capital gains tax and would therefore not have a taxable event.

The infrastructure space has been ripe for deals. BlackRock bought Global Infrastructure Partners for $12.5 billion, which held $100 billion in AUM, for a percentage of 12.5% AUM. CVC Capital Partners just bought infrastructure manager DIF and General Atlantic bought Actis. All these deals could have been a potential trigger for Tetragon to solicit bids and test the market

What could the potential value of Tetragon trade at if they sell Equitix? Based on using 60% price to NAV, it could be worth $25 for upside of 61%. The stock has historically traded at 50% of NAV for the past 10 years but I would argue that a company that’s compounded NAV at 11% since IPO and is willing to sell their largest component of NAV for cash , and maybe return that cash, could see a decrease in the discount from price to NAV. Even if you use 50% there is still a bit of upside.

Thesis #2 - Explore return of capital via tender or special dividend

If/once Equitix is sold, I believe Tetragon could look to make a tender offer using the proceeds at a significant discount to NAV. Management and Tetragon employees own about 40% of the company and would be highly incentivized to see the stock price increase now. What is the use of owning such a large chunk of a significantly undervalued company if you cannot sell your shares for their true fair value? I am assuming the tender occurs at $25 because that’s the value I have if Equitix is sold. It could, if it occurs, happen at levels below $25 which would be even more accretive to NAV. But assuming a tender is done at $25, it could result in 80% upside.

Thesis #3 - Potential IPO of Ripple Labs

This is where the thesis gets really interesting. I’ll preface by saying that I am in no way a crypto expert but I like situations with extreme optionality on the upside, even if there are different event paths that could occur. The late grate Michael Price called this the steak and sizzle approach. Focus on the steak and get the sizzle for free.

In 2019, Tetragon made a Series C preferred equity investment in Ripple Labs for $150 million with the option of Ripple redeeming their investment if it was ruled that XRP was a security on a go-forward basis. The SEC sued Ripple in 2020 stating they had been issuing unregistered securities from the sale of XRP, which led to Tetragon suing Ripple to redeem their investment as a result of the SEC lawsuit. Tetragon’s suit was dimissed and Ripple decided to buyout the Series C preferred back anyways in 2021. Tetragon then purchased Series A and B preferred of Ripple on the secondary market. While they have never disclosed the price paid or terms, there have been reports that they own about 2% of Ripple. Although not a perfect method, triangulating what Ripple is carried at on Tetragon’s balance sheet vs Ripple valuation in 2024 comes to roughly 2%:

What’s interesting about their Ripple investment though is that Ripple in January 2024 owned $25 billion worth of XRP tokens on their balance sheet at a rough price of $0.5/token when they did their tender offer for $11.3 billion last year. This meant they were buying back shares at under a 50% discount to net asset value and I believe they made another tender in 2024. And now one year later, the XRP price has gone vertical:

Sitting at just around $2.3, their XRP tokens are now worth more than $100 billion, thanks to a nearly 5-fold increase in price and the CEO of Ripple thinks the original $11.3 billion valuation of Ripple is “very outdated”. The drastic price increase is as a result of the friendly Trump administration coming into office, the resignation of Gary Gensler who was antagonistic to Ripple, Ripple only having to pay a $125 million dollar fine which was substantially below the $2 billion the SEC wanted from their lawsuit and the SEC recently approving bitcoin ETFs. Not to mention a potential US Strategic Reserve for purchasing cryptocurrencies that could come into affect.

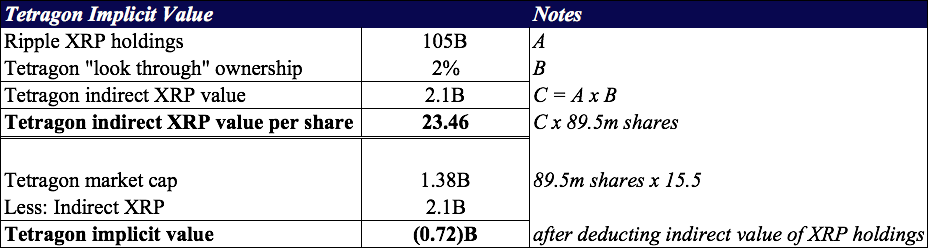

Ripple’s balance sheet isn’t public so we can’t see exactly how many tokens of XRP it holds but its around 46 billion against a total supply of 100 billion according to various news outlets. At today’s price of $2.3, Ripple owns about $105 billion XRP on balance sheet. At Tetragon’s current stock price, the “look through” ownership of their XRP holdings are about $23.46 which means Tetragon’s implicit value less their holdings is negative 720 million. Stated another way, an investment in Tetragon today means you are receiving about 3B of assets for a negative $720 million.

GAM Global Special Situations Fund has noticed the same implicit value in SBI Holdings, which is a Japanese financial services company that owns 8%-9% of Ripple and based on their look-through holdings, is trading at a negative market cap as well. They recently sent a letter to SBI you can read here. They want SBI to publish a daily figure of SBI’s lookthrough XRP holdings and to establish a public XRP coin buying program buy purchasing the coins outright to close the gap to NAV, similar to what Microstrategy has done in the US.

And Ripple itself is essentially doing somewhat of a reverse Microstrategy approach. Microstrategy issues equity at a premium to NAV and buys bitcoin whereas Ripple is just tendering for shares at a severe discount to NAV and could/should possibly sell some on balance sheet XRP and use it to repurchase more shares.

So what is the likelihood of Ripple going public and potentially releasing all of this value? Last January Ripple was looking to go public outside the U.S. because of the hostile SEC and decided to put it on hold. Since then, Gary Gensler is no longer the SEC chairman and the Trump administration has been viewed as extremely favourable to the crypto industry. Trump even issued his own coin days before he entered the white house with the first lady following suit. The CEO of Ripple has stated that going public wasn’t prioritized previously because of the prior SEC administration. With that administration now gone, experts are predicting late 2025 to 2026, potentially once the lawsuit with the SEC is finalized. I have no unique insight into when this could occur but view it as extremely positive for this investment (maybe not for society overall) that the administration is very pro crypto. While Ripple does trade on certain private markets online, coming to a precise valuation is near impossible due to no real business numbers being available. Just using a valuation of $15B, almost a 50% increase from their tender, gets to an overall stock price of Tetragon up 84%.

While the above valuation is just valuing Ripple’s potential business based on a gain from their last tender of $11.3 billion, this investment can get a bit silly on potential upside optionality if/when Ripple comes public and the market chooses to value it based on their on balance sheet XRP holdings. If the market were to value it just at todays XRP value of $105B, the upside can be quite dramatic.

And if Ripple starts trading like how the market values Microstrategy, at a multiple of their bitcoin holdings, Ripple could be worth a multiple of the 105B on balance sheet crypto holdings. The scenario above doesn’t account for the fact that the XRP token price could increase in value, or that Ripple would most likely be a highly coveted IPO by a lot of retail traders and garner a huge valuation.

Thesis #4 - Other asset sales

There is the possibility of other asset sales on top of Equitix. One of the analysts covering Tetragon thinks the BGO asset could be disposed of in the near term. While this would be viewed favourably by the market (of course depending on price and uses of the cash), it is not a main point to the overall thesis but would be most welcomed.

Potential Value Creation

Management and other executives own about 40% of the company, with the two main founders Reade Griffith and Paddy Dear owning 27%. I think they have done a relatively good job of compounding NAV since inception at 11%. One thing that does bother me is management’s aloofness on how to close the discount to NAV. On the most recent call they said “they don’t think there is a clear silver bullet to closing the discount to NAV”. I lay out some options on what I would do to close the discount at the end of this write up but with the persistent discount to NAV ongoing, upper management have the option of collecting their combined $50-$100m incentive fees per year until they retire in 5-10 years, or they have the option of creating a ton of value right up front. Based on my valuations, this could be the potential value they can create for themselves:

Risks

In all potential deals, there is the possibility of the sale falling through. If the Equitix sale doesn’t occur, it is possible this trades back down a bit and is dead money. I don’t think it should trade back down to 10, it might go down to the 11-12 range based on the markets perception that the company is willing to entertain offers for some of its assets and turn at least some of their investment NAV into cash.

What if Equitix might not get as a high a price as reported? Anything at NAV or above and turning their investment into cash is a win in my opinion as they could still use that cash to repurchase at a significant discount to NAV.

Or what if the company chooses to reinvest any proceeds from asset sales into other investments? While a bit of risk, it wouldn’t be a terrible outcome as management has shown they can grow NAV at a decent clip. However, this wouldn’t allow for larger outsized returns as outlined above in my opinion.

There is also the risk that if a down turn occurs, management can write down NAV, write it back up and double dip like they did in the GFC. I give this situation occurring low odds. Back in the GFC, management owned just loans and CLO’s, assets that were heavily affected by the crisis and most likely deserved to be written down then. Now they own a more diverse set of assets. We’ve also seen during the COVID 2020 market that their NAV actually increased, which should dispel most of this risk. The company could also face a barrage of lawsuits from investors, tainting the investment in the stock even more and thereby increasing the price to NAV of where it trades, in which management owns 40% and not giving them a path to realize their holdings at fair value.

What if Ripple doesn’t IPO or the price of XRP drops? While a lot of the upside of the investment could be tied to a Ripple IPO and their significant holdings of XRP on balance sheet, you don’t need the Ripple IPO to occur to earn a decent return in the stock. While it would be nice for Ripple to IPO and be a highly coveted asset by retailer and institutional investors, if they stay private they can still grow their value without going public. And even if their value doesn’t increase, Tetragon the stock, can still earn a good return if management liquidates some assets and repurchases shares.

Event Path If I Were Management

The first step I would take is currently what mangement is doing. Putting one of your largest holdings on the block and trying to crystalize that value. I would also sell another asset as well for further NAV uplift. Once these sales occur, I would announce a larger tender at a significant discount to NAV in order for NAV/share to grow even further, increasing management’s and investors who choose to stick around ownership further.

The next step, however unlikely, would be to convert the non-voting shares into voting. If management doesn’t sell back into the tender, they could go above 50%, thereby making the newly proposed voting shares semantics as they would now control the voting shares and eliminate some of the discount to NAV. At the same time, instill a high water mark which would further erase some of the discount to NAV. Instead of the high water being just NAV, tie it to some type of performance based measurement of shareholder value like stock price. These two steps I would do after the tender to allow a larger price to NAV gap to exist during the buyback.

Once these are done, start highlighting the Ripple investment and the indirect “look through” XRP that Tetragon now holds. This could show the market that one of the ways to play the Ripple IPO would be by owning Tetragon, thereby increasing demand for the stock.

Disclosure: Long TFG.AS, TFG.LN

Two Deep Value Special Situations Down Under; Seasoned Liquidations

I’ve recently come across two deep value situations in Australia. Both I own. The first one:

Deep Value Situation #1 - Pacific Current Group (PAC.AX)

I first became aware of Pacific in July 2023 when major shareholders Regal Partners and River Capital offered to buy them at $11.12/share. Pacific owned 16 stakes in numerous tier 1 and tier 2 boutique asset managers, one of them being at the time GQG. This was then followed by GQG Inc. (who Pacific had an investment in and is itself publicly traded) indicating they would submit a bid as well. PAC then ran a strategic process and received multiple offers. Regal withdrew their offer in September 2023 and GQG Inc. submitted a bid for $11/share all cash in November 2023 without having obtained River Capital’s support. River Capital then got back in with a bid, but this time for $10.5/share in cash. Long story short, Pacific’s strategic committee disbanded in November 2023 as it wasn’t able to get any binding offers.

What’s happened since then? Essentially a public liquidation, selling down to 11 boutiques as of August 2024.

The company has announced even more sales since August. All of these sales have changed the NAV percentage of the business dramatically:

Cash went from 2% of NAV last year to 43% as of June 2024 and this is still a growing amount. The company is now proposing to repurchase 25m shares in an off-market share buy-back, which equates to 47.9% of the shares outstanding. The shareholder vote is to take place January 30, 2025 with the 3 major shareholders representing 49% voting for it. However, they have not decided if they will tender their shares into it which creates a bit of a risk of the full buyback being used.

In order to determine potential returns, I’ve tried estimating the adjusted NAV as of this write up along with a scenario where all the shares are and aren’t bought back. There are a ton of moving pieces in the underlying NAV since last reported on June 30, 2024. Not only the recent sales but also some of the sale proceeds are to be collected over a period of a year or two. On top of that, the majority of the funds under management are reported in USD but the stock trades in AUD which must be accounted for.

Based on the assumptions above, I am getting to $14.38/share of adjusted NAV since the June 2024 NAV of $13.47/share. Below are the IRR estimates assuming a 2 month hold:

If the company is able to fulfill the full repurchase authorization, there is barely any downside with some upside depending where it trades after repurchase. The IRR on this, assuming a 2 month hold, could be a respectable 62% if it trades at a 20% discount after.

What happens if the tender is only able to be filled for half the amount allocated? Assuming only 12.5m shares can be repurchased, there is still a small IRR to be made if it trades at a 20% discount to adjusted NAV.

I’ll note that the stock is trading just below $12 so the IRRs on these numbers could be a bit greater than what I have from using the $12 beginning price. I didn’t account for any fair value uplift in potential sales as well that could provide a bit more return to the stock/NAV. Also, if the company isn’t able to get the full allocation, I imagine they could possibly do a special dividend or just sell it all/wind it down completely. The CEO is still listed as “Acting CEO” which makes you wonder what the end game is here.

The real risk that could reduce the IRR is any delay in shareholder vote and rulings from the Australian Tax Office as these have caused a delay since May. But with the vote at the end of the month I would think this happens in March when scheduled.

I am long and see this as an extremely low downside bet with some upside and the chance of earning a high IRR. The opportunity is available because it’s a small company with 3 shareholders making up almost 50% of the shares which creates limited liquidity for larger funds to enter into.

Deep Value Situation #2 - Merchant House International Limited (MHI.AX)

Merchant is a textile manufacturer that makes boots, shoes and other home products. It is based in Hong Kong and listed on the ASX but domiciled in Bermuda. It has the “ick” factor in an investment that people turn their noses up at but I think this cigar butt has one last puff. They decided in August 2024 to liquidate the company, distribute the proceeds to shareholders and delist from the ASX once they sell their last remaining property. The liquidation announcement sent the stock from $0.04 to $0.15. As you can see, the business is of extremely low quality with declining sales and net tangible assets in the prior 5 years.

Merchant has 94.2m shares outstanding and currently trades at $0.15 for a market cap of $14.13m. The average volume for the shares is 100,000 shares or $15,000 a day.

The business consisted of 3 real main businesses with a couple other small/dormant subsidiaries:

Footwear Industries of Tennessee Inc. (FIT) which was sold in 2023 for gross proceeds of $3.28m USD and net proceeds of $2.63m for its fixed assets net of liabilities. The land and buildings in this sale had a book value $US 788K and sold for profit in the sale of $1.965m USD, amongst some other small assets. The main thing to note is the property sold above book value here.

Forsan Limited (Forsan) was a 33.79% ownership in a JV with Mr. Wu Shu Xin for Tianjin Tianxing Kesheng Leather Products Company Limited based in China. This was sold on May 30, 2024 for $8.3m AUD before taxes, costs and other payments. The company completed the sale on January 9 2025 for $4.9m USD.

American Merchant Inc. Most of the value of the overall company is in this subsidiary as it holds a large piece of textile PP&E located in Bristol,VA. It was recently shut down as of September 30, 2024 and to be put up for sale. According to their website they have invested more than $24m in state-of-the-art equipment in the plant. This article also gives some background of the facility, equipment owned and its sale. Below is a picture of the plant:

And a location of the factory from google earth:

4. Various subsidiaries - Pacific Bridges Enterprises Inc and Loretta Lee Limited. I am assuming Pacific Bridges is not worth anything. Loretta Lee Limited currently has a contingent liability of US$994,996 that must be returned plus interest owing from a court case.

The company has recently stated in their September 2024 Half-Year report release in late November that they have received expressions of interest from potential buyers and expects the sale process to be complete within 12 months.

Liquidation Proceeds

So what can you expect to get in the liquidation? I lay out a bear, base and bull case with various assumptions on the amount the plant will sell for. Even in a draconian scenario where it only goes for 50% of stated book value, you would still get a decent return.

I haven’t been able to really find any precedent transactions for this type of asset in the area. But as stated earlier they were able to sell their FIT division for above book value. In 2022 they sold their 30% interest in Jiahua for $AUD 3.3m and it was carried on their books at $AUD 1.9m. And in April 2021 they disposed of their subsidiary Carsan for net proceeds of $AUD 21m for roughly 1x revenues and 3.8x book value based off my calculations from the segment’s book value of $AUD 5.5m as disclosed on page 20-21 of the 2021 annual report. In my model I have 4 boards of directors but one resigned in August but I left 4 in to be conservative.

The CEO owns 61.2m shares or 65% of the company and should be highly incentivized to get the best price and the company liquidated as quick as possible.

Many things can go wrong with this investment:

The sale process can drag out which will eat into your IRR.

The plant may not sell for 50% above book or might not be able to find a buyer thereby wiping out your downside. These are not very “attractive” assets but they have garnered some interest as per the release and the company has a history of selling these types of assets.

The company might have to sell off pieces of equipment each before they can sell the entire plant. This would prolong the amount of time it takes to liquidate.

Management can change their mind about liquidating and hoard the cash for an acquisition.

Management can pilfer the company by paying out large salaries leaving shareholders left with nothing. This risk is the one that I worry about the most because you are always on the outside looking in in non-control liquidations like these in foreign jurisdictions. However, the release did state they wish to distribute the proceeds out to shareholders so hopefully there is no pound of flesh taken before that occurs.

I have a small position in this because while I don’t love the asset they have to sell, their history of getting north of book provides such a large discount to fair market value that you are well compensated for that risk. It also helps that this situation is uncorrelated with the overall market.

This investment brings me to a topic I’ve read about and think is extremely interesting in liquidation scenarios.

Seasoned liquidations

I read about a technique called “seasoned liquidations” in the book Merger Masters: Tales of Arbitrage. In the chapter about John Bader from Halycon Capital Management, he explains that a seasoned liquidation is one where the assets have actually been sold and are just sitting in cash waiting to be distributed to shareholders. All that needs to be accounted for in this situation is claims the company still has to pay out and the timeline. I think this technique is extremely smart, especially in situations where the assets have not been sold yet and it can be hard to put a value on the assets. There might not be as much upside using a seasoned liquidation approach, but your risk decreases dramatically because you are not relying on valuing the remaining asset to be sold. Just the cash in the register essentially.

This situation can be applied in the Merchant House pitch above due to the nature of the remaining asset. Once the price of that asset is sold, your risk of capital impairment would go dramatically down as you will be in a better position to see all the cash less payments to be made, the timeline of receiving your capital back and the stock price. Of course the stock will move before you are able to purchase it but the idea is to squeak out a few percentage points of return with minimal downside as it will most likely trade at a discount to full value. It is a very valid approach to liquidation investing and can be used in your special situation arsenal.